For years, myself, and many others have thought that interest rates were the predictor of housing prices. Fast forward to post COVID where interest rates have doubled and yet housing prices remain high and are still trending higher in many markets. What other metric should we watch to see where housing prices are heading? Hint, check out the chart above.

Looking at the data, there is an interesting trend occurring due to the wealth effect of the stock market. The percentage of all cash buyers increased especially for vacation/second homes over the last 5 years. Why are cash buyers increasing and what does this mean for real estate prices? Furthermore, how is the wealth effect impacting prices? What does the stock market mean for housing prices this year and over the next decade?

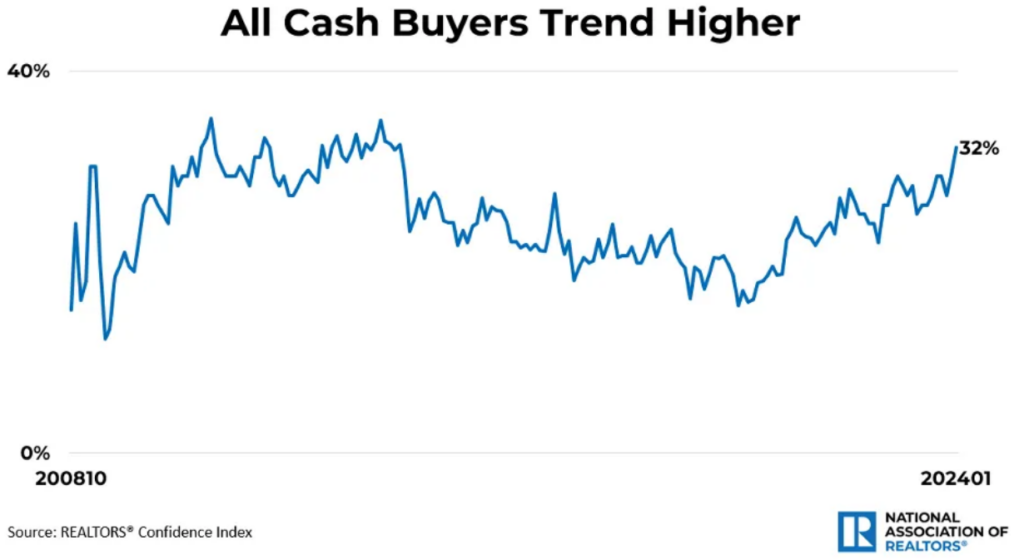

All Cash buyers increase

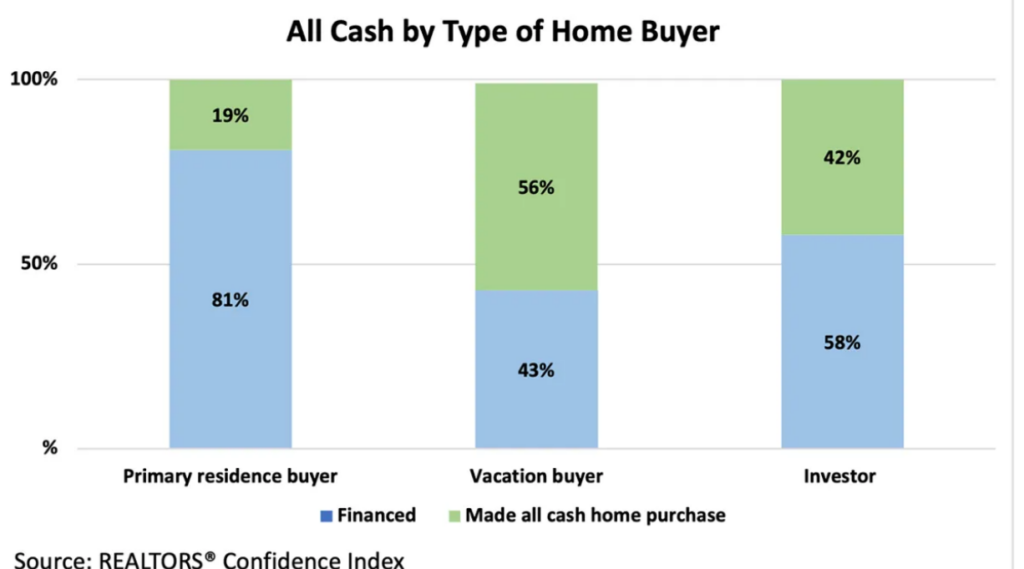

While mortgage interest rates have more than doubled in recent years, the share of all cash buyers is growing. all cash home buyers have trended up significantly in recent months. Since October 2022, all cash home buyers who did not finance their recent home purchase have been more than one-quarter of the real estate market. In January 2024, all cash buyers now stand at 32% of home sales. The last time the share of all cash buyers was this high was June 2014. From the chart it is easy to see why many vacation markets have been supercharged as over half of the buyers are cash. This also explains why interest rates have had less of an impact with so many properties being bought with cash.

High correlation between stock market and real estate prices

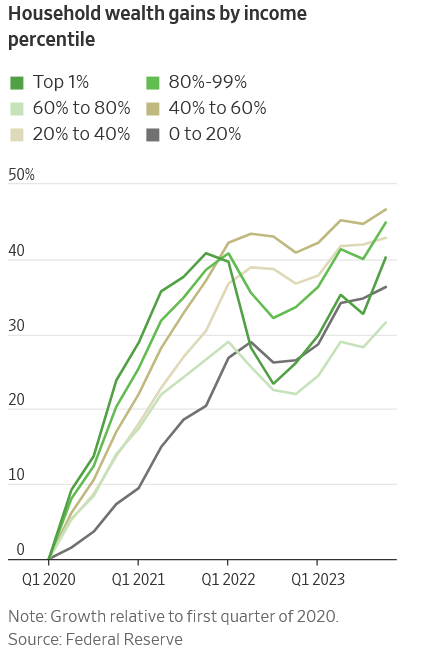

Along with cash buyers, the stock market has been on a tear until recently. In the past, interest rates were the primary driver of real estate prices, as rates moved substantially higher, property values dropped. This has not occurred in this cycle because as rates moved substantially higher so did almost every other asset from stocks to bitcoin to many commodities. This has created a substantial wealth effect for most Americans as shown in the chart below. The amount of wealth created in this cycle is astounding.

This wealth has allowed more people to buy properties all cash and/or absorb higher prices. As the stock market remains high so have housing prices and the correlation between the two has only increased during the post pandemic cycle.

High real estate prices creating a positive reinforcement loop

Along with the stock market, the high value of houses themselves is now keeping prices high creating a loop effect. If you are going to sell your house, you can get substantially more than five years ago, this will enable many buyers to buy their next house in cash especially if they move to a lower cost area. This in turn is driving up prices in less expensive markets as there is more demand from other areas.

Interest rates higher for longer than market thinks

Housing is the number one driver of inflation comprising over a third of the consumer price index. As housing prices stay higher along with rents, it will be difficult to see a major reset in inflation. The market is currently pricing in several cuts to rates later this year. I don’t foresee a huge movement in rates based on the wealth effect highlighted above.

Prices will continue to stay high until stock market reset

Prices of houses will continue near their peak until there is a stock market reset and people “feel” less wealthy. Currently interest rates today are likely not high enough for this to occur which will keep the federal reserve on a path for higher for longer until there is a major reset in asset prices. Without a reset in the stock market and in turn housing the economy will be stuck where it is today for a bit longer. The million dollar question is if this recent hiccup in the stock market is a big enough reset to radically alter real estate’s trajectory heading into the spring season?

Big changes in long-term forecasts for the stock market

The headline says it all “ Decade of big S&P 500 gains is over”. The predictions for the stock market are pretty grim:

” US stocks are unlikely to sustain their above-average performance of the past decade as investors turn to other assets including bonds for better returns, Goldman Sachs Group Inc. strategists said.

The S&P 500 Index is expected to post an annualized nominal total return of just 3% over the next 10 years, according to an analysis by strategists including David Kostin. That compares with 13% in the last decade, and a long-term average of 11%.

They also see a roughly 72% chance that the benchmark index will trail Treasury bonds, and a 33% likelihood they’ll lag inflation through 2034.”

Essentially real estate rode the asset appreciation wave of the stock market up and is now married to the new reality of substantially lower returns. Based on the predictions of Goldman Sachs this would correlate to a similar scenario for real estate with returns averaging around 3% over the next 10 years, this is a huge drop from the 20%+ we saw some years during the Covid boom.

More correlation means greater downside risk

Although the wealth effect has created huge positives for the housing market with stable to rising prices in face of higher interest rates, the party cannot last forever. Unfortunately we have already seen the upside over the last 10 years or so.

The downside risk is much more likely. With the huge run ups in wealth and the historically strong stock market there is a much higher correlation between housing and the stock market. As one goes down so will the other. As we have seen throughout the years in economics, high correlations are great when markets are increasing but when the winds change and there is a reset, the downside risk is amplified.

Currently with asset values wobbling we haven’t seen much change in real estate values yet, but the data says that change is underfoot. The increased volatility in the stock market should be a wakeup call as the stock market does not go up into perpetuity. Furthermore, values are extremely lofty based on any historical metric which further enhance the risk of an even larger correction.

A reset in the stock market will ultimately lead to a much greater reset in real estate values than in the past due to the higher correlation. The million dollar question is when will this occur and how much will housing prices drop. My gut says that later this year or early next year, the reset will occur as the everything rally in stocks and other assets peters out, but the real story is that the decade of huge real estate gains is likely over just like we will see in the stock market which means housing prices are basically going to stay at best case even with inflation (basically 2-3% a year for the next 10 years) for the next decade or worst case have a reset and underperform inflation.

On a side note, remember that real estate is market specific so certain cities will perform better than others due to demographic shifts, price points, etc… that will alter individual real estate markets. More expensive markets, like Denver will be hit harder than other markets as the average price is over 600k meaning many of the prospective buyers at this price point likely have substantial exposure to the stock market.

Regardless of the market, the days of all assets rising in harmony is starting to reverse as we can see in the stock market. There will be opportunities but it will be considerably more difficult than the past 10 years where all you had to do was buy a property with 4 walls and you could make money.

Additional Reading/Resources:

- https://www.nar.realtor/blogs/economists-outlook/the-share-of-all-cash-buyers-highest-since-2014-at-32-of-all-buyers

- https://www.bloomberg.com/news/articles/2024-10-21/s-p-500-s-decade-of-big-gains-is-over-goldman-strategists-say?srnd=homepage-americas

- https://www.fairviewlending.com/stock-market-reset-impact-on-real-estate/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends . I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games).

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender