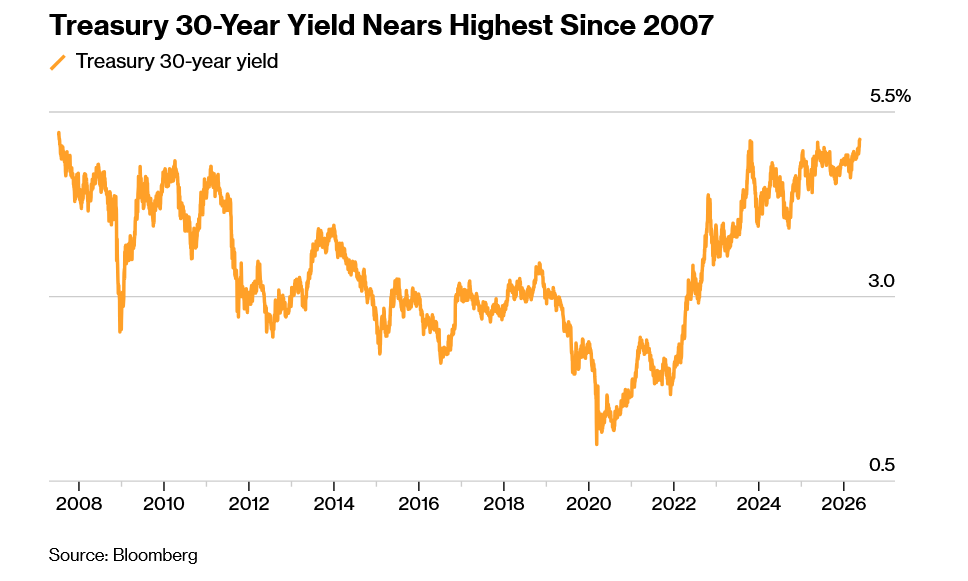

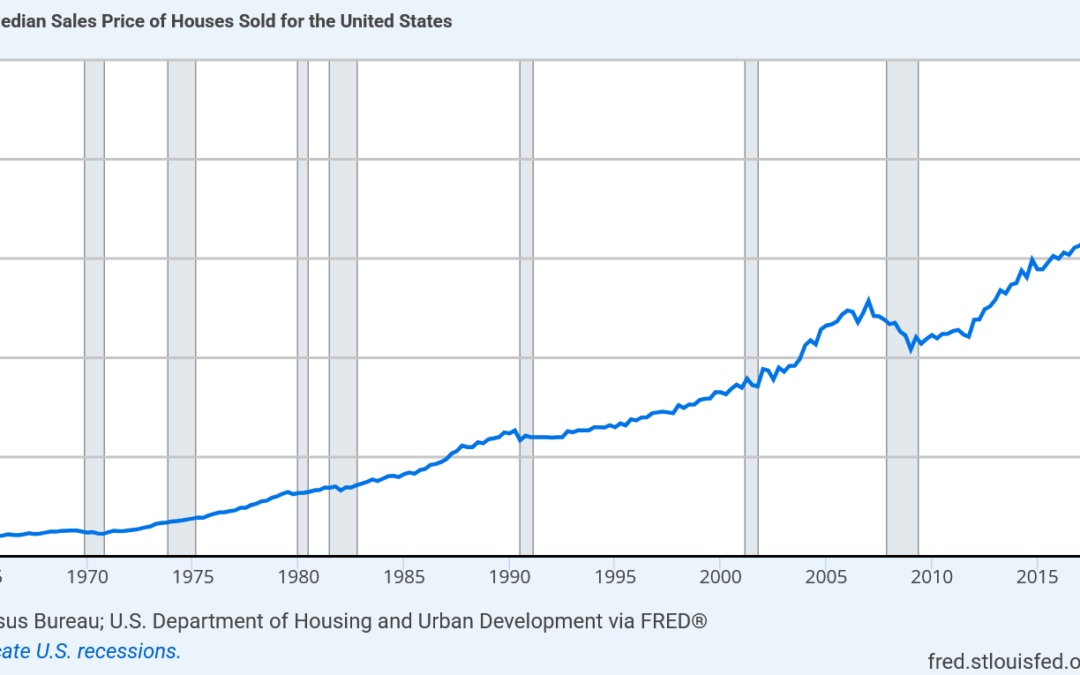

The May inflation report is in, rising to the highest level in 3 years. Look at the chart above, out of nowhere yields have surged to almost 20-year highs and predictions exceeding 6%. The market is suddenly catching on that we have an inflation...

What does May inflation mean for interest rates and real estate?

read more